A system to allow anyone - from the piano teacher plumber - to accept payments by credit card, using a smartphone terminal. And 'This is the gimmick Square, start-up based in San Francisco at the end of 2009 created by Jack Dorsey, Twitter co-founder, along with Evan Williams and Biz Stone. The technology is so easy to leave open-mouthed: just attach a small square in the audio jack of an Apple (iPhone, iPad or iPod Touch) or Android.

With a few adjustments, the payment is made, without having to sign any contract or buy the special machine, the famous Pos or "point of sale." For now the system is limited to the United States and its prevalence is still marginal, but analysts are confident of its success. Sure liked the idea very large investors like Sequoia Capital, Khosla Ventures and JP Morgan Chase, which have made this a start-up Diamond Head in Silicon Valley.

Easy to see why: potentially, in fact, that white square opens up a huge amount of information, the most valuable asset markets of the twenty-first century. Square: from idea to product. As explained by Technology Review in a special entitled "The New Money," Square "daughter" of two trends have emerged in recent years: on the one hand, the proliferation of smartphones and other mobile devices, on the other hand the reduction of cash payments with respect to those with a credit card.

For Dorsey, now 34 years old, this was (also) a kind of revenge for what many in Silicon Valley, perceived as an injustice: his ouster in October 2008, the CEO of Twitter, for the benefit of the richest and most famous co-founder, Evan Williams. In the new adventure Dorsey has thrown together the entrepreneur Jim McKelvey, the first commission, at age 15, a software CD-ROM.

"It all started on Christmas 2008," says the CEO of Square today. "McKelvey had started working as a glass blower. One day he phoned me, telling me how he had lost a deal worth $ 3,000 because he could not prosecute an American Express. We were talking from iPhone to iPhone at some point I was struck by the thought that, in reality, he was holding almost all the hardware it needed to complete the sale.

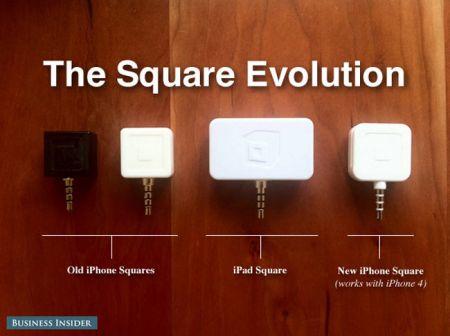

" How it works. With the help of a programmer, the two have worked to create Square: a magnetic reader in like a white square (2.5 centimeters) to be inserted in the audio jack of your smartphone. Then I moved on to writing the software and its application for the iPhone. The system works extremely simple: After "crawling" the paper, the reader turns the magnetic data into electrical signals, the application at this point, translates the information in an encrypted file and mail servers to Square.

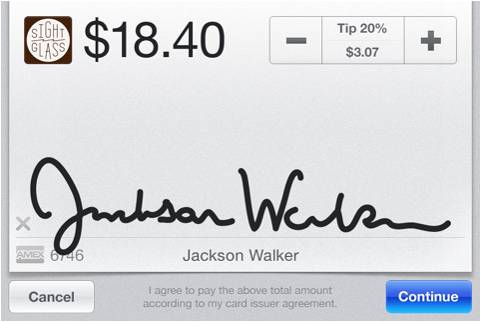

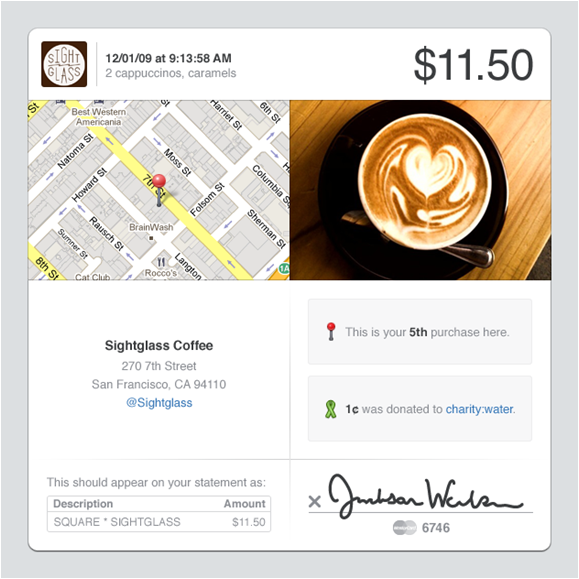

And 'here, finally, that the transaction is completed through the global network. The person making the purchase is required to sign directly on the phone, and then decide if you like a receipt via e-mail or text message. Create an account and become a part of the "non-tour" is just as easy: just download the application by the Apple App Store or (new in the last days) from the Android Market, install it on your device, accept the terms of service and enter some personal data.

Et voila: the box arrives by mail within 48 hours, but right now you can accept payments by typing on the iPhone or the Droid few, essential information on the paper and its owner. Costs. Of course, convert to Square has its cost: the system, in fact, "eat" 2.75% of each transaction, a figure that includes the company's earnings and reimbursement for credit card companies.

In absolute terms, the cost may seem higher than the activation and operation of a terminal "traditional", but - at least in the U.S. market - it is not so predictable. "There are several reasons why ordinary people do not accept credit cards," explains Dorsey. "The payment system is extraordinarily complex, opaque and expensive.

First you have to apply for a merchant account through a bank or an independent organization. The only question involves a credit check, which can take up to one week. Then you have to buy the 'hardware, and for wireless equipment is around $ 900. Not to mention the monthly cost: between 15 and 25 dollars, even if customers do not buy anything.

" For all these reasons, adds Keith Rabois, COO of start-up and former business manager for PayPal and LinkedIn, "agrees traders Square is a way to enhance their business." Some numbers. To date, Square has more than 200,000 accounts and processes a number between 2 and 10 million dollars a week.

The pilot program, launched in early 2010, took part in 50,000. From the official release of the system, which took place last October until December, users increased by 100,000. Others were added only 65,000 in January. But the ambitions of the creators of Square are very different: to process transactions for one billion dollars only in 2011.

Vast, indeed, is the catchment area it seeks to the start-up: as explained Rabodis who belong to "the 27 million U.S. businesses that can not accept payments by credit card, as well as the 33 millions of Americans who sell goods and services only occasionally and 7 million merchants, while already possessing a terminal, they want a more efficient system for mobile payment.

As for the future, the intention is to start exporting the payment system outside of North America as early as 2012, although plans are still secret. The competition - for now - is not a problem. Recently, in fact, large companies such as VeriFone, Intuit and TF Payments have launched similar products (called, respectively, payware Mobile, GoPayment Focus and Pay) that allow users to accept credit cards by setting the magnetic readers to smartphones.

In these cases, however, it is just new hardware, and not a completely new system of payments: individual sellers, in fact, they still require a specific account and then go through the banks or their brokers. If it rains "Business angels". The potential of the area have not escaped the many gold diggers - or rather, what could become gold - that roam the Bay of San Francisco.

In recent months, in fact, Square has seen jumping through the roof investment both by individual business angels from the venture capital giants. In January, for example, Sequoia Capital and Khosla Ventures have joined the board of directors of the company, carrying over 27.5 million dollars and the experience of Roelof Botha, who was also former head of Paypal.

So, in just over a year, the company has grown from a valuation of $ 40 million - in December 2009 - to over 240 million today (source: Wall Street Journal). The flip side of mobile payment. Because of its simplicity and the fact that it potentially open to any person with a bank account and smartphones, Square acts as the antagonist of the twin-based mobile payment technology, Near Field Communication (NFC), where the customer pays for using your phone to instead of a credit card.

On the one hand you might think that, in Silicon Valley, some do not believe much in this turning-technology economy ", according to a recent survey by Aite Group, should make the smartphone" the only form of payment by 2015 ". Or perhaps, more simply, they are two complementary trend towards a common destiny, path parallel to the emerging realities Square and giants like Google, from the outset in the front row for the NFC.

Meanwhile, in the wake of the application last month has made 2.0 or Starbucks coffee shop, one thing is certain: even if you can not predict the timing of these technologies evolve, the money from first-hand - or to listen to, how did the Harpagon Moliere starring Alberto Sordi - will become increasingly rare.

With a few adjustments, the payment is made, without having to sign any contract or buy the special machine, the famous Pos or "point of sale." For now the system is limited to the United States and its prevalence is still marginal, but analysts are confident of its success. Sure liked the idea very large investors like Sequoia Capital, Khosla Ventures and JP Morgan Chase, which have made this a start-up Diamond Head in Silicon Valley.

Easy to see why: potentially, in fact, that white square opens up a huge amount of information, the most valuable asset markets of the twenty-first century. Square: from idea to product. As explained by Technology Review in a special entitled "The New Money," Square "daughter" of two trends have emerged in recent years: on the one hand, the proliferation of smartphones and other mobile devices, on the other hand the reduction of cash payments with respect to those with a credit card.

For Dorsey, now 34 years old, this was (also) a kind of revenge for what many in Silicon Valley, perceived as an injustice: his ouster in October 2008, the CEO of Twitter, for the benefit of the richest and most famous co-founder, Evan Williams. In the new adventure Dorsey has thrown together the entrepreneur Jim McKelvey, the first commission, at age 15, a software CD-ROM.

"It all started on Christmas 2008," says the CEO of Square today. "McKelvey had started working as a glass blower. One day he phoned me, telling me how he had lost a deal worth $ 3,000 because he could not prosecute an American Express. We were talking from iPhone to iPhone at some point I was struck by the thought that, in reality, he was holding almost all the hardware it needed to complete the sale.

" How it works. With the help of a programmer, the two have worked to create Square: a magnetic reader in like a white square (2.5 centimeters) to be inserted in the audio jack of your smartphone. Then I moved on to writing the software and its application for the iPhone. The system works extremely simple: After "crawling" the paper, the reader turns the magnetic data into electrical signals, the application at this point, translates the information in an encrypted file and mail servers to Square.

And 'here, finally, that the transaction is completed through the global network. The person making the purchase is required to sign directly on the phone, and then decide if you like a receipt via e-mail or text message. Create an account and become a part of the "non-tour" is just as easy: just download the application by the Apple App Store or (new in the last days) from the Android Market, install it on your device, accept the terms of service and enter some personal data.

Et voila: the box arrives by mail within 48 hours, but right now you can accept payments by typing on the iPhone or the Droid few, essential information on the paper and its owner. Costs. Of course, convert to Square has its cost: the system, in fact, "eat" 2.75% of each transaction, a figure that includes the company's earnings and reimbursement for credit card companies.

In absolute terms, the cost may seem higher than the activation and operation of a terminal "traditional", but - at least in the U.S. market - it is not so predictable. "There are several reasons why ordinary people do not accept credit cards," explains Dorsey. "The payment system is extraordinarily complex, opaque and expensive.

First you have to apply for a merchant account through a bank or an independent organization. The only question involves a credit check, which can take up to one week. Then you have to buy the 'hardware, and for wireless equipment is around $ 900. Not to mention the monthly cost: between 15 and 25 dollars, even if customers do not buy anything.

" For all these reasons, adds Keith Rabois, COO of start-up and former business manager for PayPal and LinkedIn, "agrees traders Square is a way to enhance their business." Some numbers. To date, Square has more than 200,000 accounts and processes a number between 2 and 10 million dollars a week.

The pilot program, launched in early 2010, took part in 50,000. From the official release of the system, which took place last October until December, users increased by 100,000. Others were added only 65,000 in January. But the ambitions of the creators of Square are very different: to process transactions for one billion dollars only in 2011.

Vast, indeed, is the catchment area it seeks to the start-up: as explained Rabodis who belong to "the 27 million U.S. businesses that can not accept payments by credit card, as well as the 33 millions of Americans who sell goods and services only occasionally and 7 million merchants, while already possessing a terminal, they want a more efficient system for mobile payment.

As for the future, the intention is to start exporting the payment system outside of North America as early as 2012, although plans are still secret. The competition - for now - is not a problem. Recently, in fact, large companies such as VeriFone, Intuit and TF Payments have launched similar products (called, respectively, payware Mobile, GoPayment Focus and Pay) that allow users to accept credit cards by setting the magnetic readers to smartphones.

In these cases, however, it is just new hardware, and not a completely new system of payments: individual sellers, in fact, they still require a specific account and then go through the banks or their brokers. If it rains "Business angels". The potential of the area have not escaped the many gold diggers - or rather, what could become gold - that roam the Bay of San Francisco.

In recent months, in fact, Square has seen jumping through the roof investment both by individual business angels from the venture capital giants. In January, for example, Sequoia Capital and Khosla Ventures have joined the board of directors of the company, carrying over 27.5 million dollars and the experience of Roelof Botha, who was also former head of Paypal.

So, in just over a year, the company has grown from a valuation of $ 40 million - in December 2009 - to over 240 million today (source: Wall Street Journal). The flip side of mobile payment. Because of its simplicity and the fact that it potentially open to any person with a bank account and smartphones, Square acts as the antagonist of the twin-based mobile payment technology, Near Field Communication (NFC), where the customer pays for using your phone to instead of a credit card.

On the one hand you might think that, in Silicon Valley, some do not believe much in this turning-technology economy ", according to a recent survey by Aite Group, should make the smartphone" the only form of payment by 2015 ". Or perhaps, more simply, they are two complementary trend towards a common destiny, path parallel to the emerging realities Square and giants like Google, from the outset in the front row for the NFC.

Meanwhile, in the wake of the application last month has made 2.0 or Starbucks coffee shop, one thing is certain: even if you can not predict the timing of these technologies evolve, the money from first-hand - or to listen to, how did the Harpagon Moliere starring Alberto Sordi - will become increasingly rare.

- La Rivoluzione che non Sappiamo Pensare (26/11/2010)

- Smartphone Visa Readers (UPDATE) - Square Device and App Make Mobile Paying Possible (GALLERY) (04/02/2011)

- Square Drops Fees, Everybody Loves Square (22/02/2011)

- Can Square make money with its new pricing? (23/02/2011)

- Hey Square-Enix, Samurai Eleven looks familiar (23/02/2011)

No comments:

Post a Comment